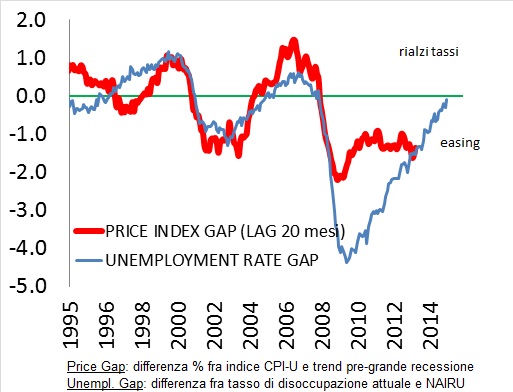

Il mercato del lavoro USA tira come un bue imbizzarrito, non c’è altro da dire. A nulla serve soffermarsi sugli indicatori rimasti indietro su cui pesano ancora fattori strutturali della crisi del 2008-09. Lo stesso tasso di sottooccupazione U-6 è entrato nell’area 11%-10.5% coerente con tassi di intervento più elevati (Congiuntura del 30 gennaio). Cosa preclude allora Janet Yellen dall’iniziare immediatamente la politica monetaria restrittiva rimandando la data dell’ormai famoso “lift off”?

Fino ad oggi la Fed non ha percepito una dinamica salariale tale da intervenire. Difatti il gap sui prezzi al consumo (Price Gap) suggerirebbe di mantenere inalterata l’attuale politica monetaria ultraespansiva ancora fino a 2016 inoltrato. Cosa sta cambiando? Il tasso di disoccupazione prossimo alla “piena occupazione” (NAIRU) sarebbe anticipatore di una ripresa dei prezzi e di salari futura (nell’arco dei prossimi 15/20 mesi) tale da ridurre il gap creatosi nell’indice dei prezzi al consumo nella fase post grande recessione. Ciò porterebbe a collocare la data del lift off intorno a settembre 2015. Ormai alla Fed è iniziato il conto alla rovescia per il primo rialzo dei tassi da giugno del 2006.

LI_UK,

hard and straight, as ever!

Honestly, in the evaluation of the various reports and several writings, as well as statistics, I expect/ed as early as July.

But Fisher leaves the stage and rings the bells … “for next year”!

Pre-tactical of the daisy?!? Cocktail-mood in NY!

_^ In the real world, one never sees the smooth, moderately sized unemployment increases that our simple mathematical models so readily generate.

A recessionary dynamic kicks in whenever the unemployment rate rises by more than a few tenths of a percentage point.

The problem with overshooting full employment to any significant degree is that it has always set the stage for a new recession. Gaining weight (reducing the unemployment rate) is easy.

Attempts to lose weight (to stem overheating of the economy) seem always to get out of control and land us in the hospital.

Every time the Fed has tightened policy after achieving full employment, it has driven the economy into recession.

It’s because of this dynamic, and my desire to prolong the current expansion, that I have argued that we should begin reducing policy accommodation earlier than many of my colleagues on the FOMC appear to prefer.

There’s every indication that solid, above-potential growth in employment and output is going to continue through the summer of 2015.

The unemployment rate is likely to reach the bottom of the range of natural-rate estimates within that time frame.

So if we are serious about limiting full-employment overshoot, I posit that prompt action to scale back policy accommodation is likely to prove imperative.

The idea that we can substitute a steeper future funds-rate path for an early liftoff seems risky to me.

I would rather the FOMC raise rates early and gradually than late and steeply.

The credibility of a “later and steep” policy strategy is suspect, it seems to me. Isn’t it possible – even likely – that the public will interpret a decision to defer liftoff as a signal that the committee is generally “dovish” and generally disinclined to raise rates?

In other words, mightn’t the public see the choice as between “earlier and gradual” and “later and gradual” rather than between “earlier and gradual” and “later and steep?”.

I have felt that were we to begin liftoff – (…) – earlier in 2015, markets would have more confidence about the “gradual” in “earlier and gradual”.

Otherwise, as some of my colleagues have stated publicly, if we were to defer liftoff until, say, December 2015 but plan to raise rates quickly thereafter, people have to wait until January 2016 to determine whether the FOMC is serious.

Early and gradual is quickly verified.

Later and steep requires a high level of trust. It is certainly no stretch to think that the public might not completely buy into the “steep” in “later and steep”.

And what about the incentive to renege? January 2016 arrives.

Suppose that the public has, in fact, not bought into the FOMC’s promises of a steeper funds rate path.

What if the Fed’s surveys of market operators and dealers reveal that financial bets and commitments have been made such that a move to raise rates appears likely to incite financial market turbulence?

Might future policymakers then be strongly tempted to back down? ^_

l- – – – –

R. W. Fisher (Federal Reserve Bank of Dallas, Pr. and CEO, the), [Speech] “Janet Yellen is no Mae West!” – Remarks before Rice University’s Baker Institute for Public Policy Founding Director’s lecture series, Houston: March 9, 2015

http://www.dallasfed.org/assets/documents/news/speeches/fisher/2015/fs150309.pdf [Pp. 10-11 / 14]

– – – – -l

December 2015 and January 2016 arrive (knocking on wood, to have a good luck)!

Doing the HORNS … uè _I-I_ tiè!!!

Surfer [We have to wait until the end of April – also to understand the British side of the castle, now – so!]

always a pleasure…

“Doing the HORNS”

LOLZ